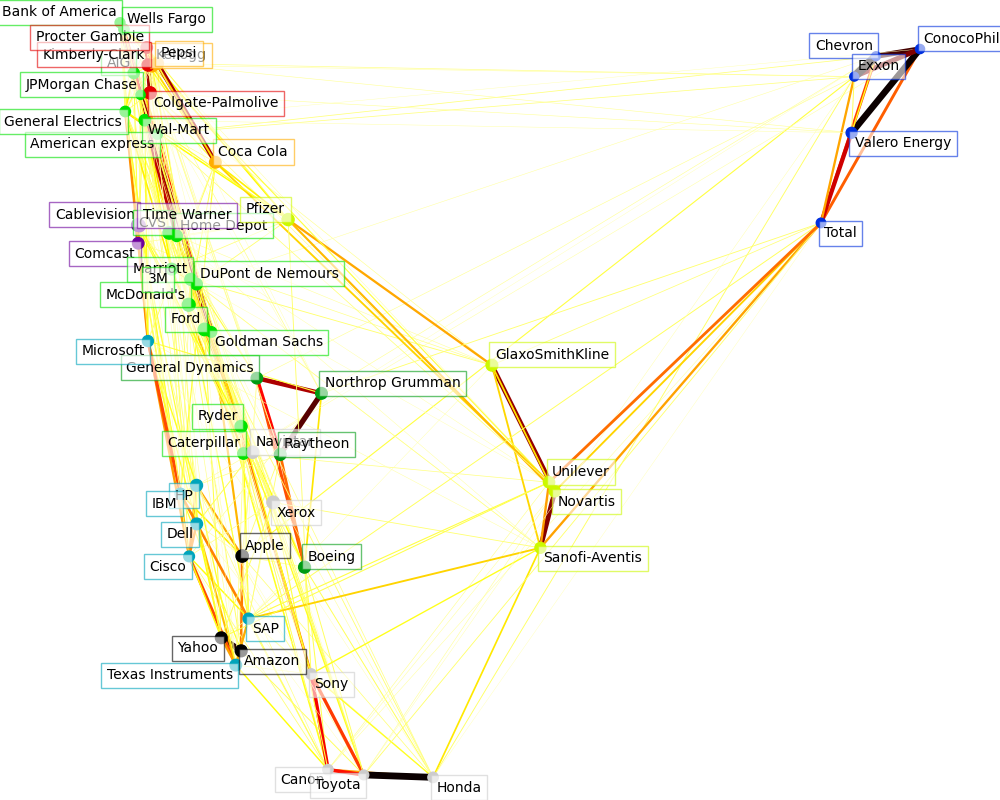

Visualizing the stock market structure#

This example employs several unsupervised learning techniques to extract the stock market structure from variations in historical quotes.

The quantity that we use is the daily variation in quote price: quotes that are linked tend to fluctuate in relation to each other during a day.

# Author: Gael Varoquaux gael.varoquaux@normalesup.org

# License: BSD 3 clause

Retrieve the data from Internet#

The data is from 2003 - 2008. This is reasonably calm: (not too long ago so that we get high-tech firms, and before the 2008 crash). This kind of historical data can be obtained from APIs like the data.nasdaq.com and alphavantage.co.

import sys

import numpy as np

import pandas as pd

symbol_dict = {

"TOT": "Total",

"XOM": "Exxon",

"CVX": "Chevron",

"COP": "ConocoPhillips",

"VLO": "Valero Energy",

"MSFT": "Microsoft",

"IBM": "IBM",

"TWX": "Time Warner",

"CMCSA": "Comcast",

"CVC": "Cablevision",

"YHOO": "Yahoo",

"DELL": "Dell",

"HPQ": "HP",

"AMZN": "Amazon",

"TM": "Toyota",

"CAJ": "Canon",

"SNE": "Sony",

"F": "Ford",

"HMC": "Honda",

"NAV": "Navistar",

"NOC": "Northrop Grumman",

"BA": "Boeing",

"KO": "Coca Cola",

"MMM": "3M",

"MCD": "McDonald's",

"PEP": "Pepsi",

"K": "Kellogg",

"UN": "Unilever",

"MAR": "Marriott",

"PG": "Procter Gamble",

"CL": "Colgate-Palmolive",

"GE": "General Electrics",

"WFC": "Wells Fargo",

"JPM": "JPMorgan Chase",

"AIG": "AIG",

"AXP": "American express",

"BAC": "Bank of America",

"GS": "Goldman Sachs",

"AAPL": "Apple",

"SAP": "SAP",

"CSCO": "Cisco",

"TXN": "Texas Instruments",

"XRX": "Xerox",

"WMT": "Wal-Mart",

"HD": "Home Depot",

"GSK": "GlaxoSmithKline",

"PFE": "Pfizer",

"SNY": "Sanofi-Aventis",

"NVS": "Novartis",

"KMB": "Kimberly-Clark",

"R": "Ryder",

"GD": "General Dynamics",

"RTN": "Raytheon",

"CVS": "CVS",

"CAT": "Caterpillar",

"DD": "DuPont de Nemours",

}

symbols, names = np.array(sorted(symbol_dict.items())).T

quotes = []

for symbol in symbols:

print("Fetching quote history for %r" % symbol, file=sys.stderr)

url = (

"https://raw.githubusercontent.com/scikit-learn/examples-data/"

"master/financial-data/{}.csv"

)

quotes.append(pd.read_csv(url.format(symbol)))

close_prices = np.vstack([q["close"] for q in quotes])

open_prices = np.vstack([q["open"] for q in quotes])

# The daily variations of the quotes are what carry the most information

variation = close_prices - open_prices

Fetching quote history for 'AAPL'

Fetching quote history for 'AIG'

Fetching quote history for 'AMZN'

Fetching quote history for 'AXP'

Fetching quote history for 'BA'

Fetching quote history for 'BAC'

Fetching quote history for 'CAJ'

Fetching quote history for 'CAT'

Fetching quote history for 'CL'

Fetching quote history for 'CMCSA'

Fetching quote history for 'COP'

Fetching quote history for 'CSCO'

Fetching quote history for 'CVC'

Fetching quote history for 'CVS'

Fetching quote history for 'CVX'

Fetching quote history for 'DD'

Fetching quote history for 'DELL'

Fetching quote history for 'F'

Fetching quote history for 'GD'

Fetching quote history for 'GE'

Fetching quote history for 'GS'

Fetching quote history for 'GSK'

Fetching quote history for 'HD'

Fetching quote history for 'HMC'

Fetching quote history for 'HPQ'

Fetching quote history for 'IBM'

Fetching quote history for 'JPM'

Fetching quote history for 'K'

Fetching quote history for 'KMB'

Fetching quote history for 'KO'

Fetching quote history for 'MAR'

Fetching quote history for 'MCD'

Fetching quote history for 'MMM'

Fetching quote history for 'MSFT'

Fetching quote history for 'NAV'

Fetching quote history for 'NOC'

Fetching quote history for 'NVS'

Fetching quote history for 'PEP'

Fetching quote history for 'PFE'

Fetching quote history for 'PG'

Fetching quote history for 'R'

Fetching quote history for 'RTN'

Fetching quote history for 'SAP'

Fetching quote history for 'SNE'

Fetching quote history for 'SNY'

Fetching quote history for 'TM'

Fetching quote history for 'TOT'

Fetching quote history for 'TWX'

Fetching quote history for 'TXN'

Fetching quote history for 'UN'

Fetching quote history for 'VLO'

Fetching quote history for 'WFC'

Fetching quote history for 'WMT'

Fetching quote history for 'XOM'

Fetching quote history for 'XRX'

Fetching quote history for 'YHOO'

Learning a graph structure#

We use sparse inverse covariance estimation to find which quotes are correlated conditionally on the others. Specifically, sparse inverse covariance gives us a graph, that is a list of connections. For each symbol, the symbols that it is connected to are those useful to explain its fluctuations.

from sklearn import covariance

alphas = np.logspace(-1.5, 1, num=10)

edge_model = covariance.GraphicalLassoCV(alphas=alphas)

# standardize the time series: using correlations rather than covariance

# former is more efficient for structure recovery

X = variation.copy().T

X /= X.std(axis=0)

edge_model.fit(X)

Clustering using affinity propagation#

We use clustering to group together quotes that behave similarly. Here, amongst the various clustering techniques available in the scikit-learn, we use Affinity Propagation as it does not enforce equal-size clusters, and it can choose automatically the number of clusters from the data.

Note that this gives us a different indication than the graph, as the graph reflects conditional relations between variables, while the clustering reflects marginal properties: variables clustered together can be considered as having a similar impact at the level of the full stock market.

from sklearn import cluster

_, labels = cluster.affinity_propagation(edge_model.covariance_, random_state=0)

n_labels = labels.max()

for i in range(n_labels + 1):

print(f"Cluster {i + 1}: {', '.join(names[labels == i])}")

Cluster 1: Apple, Amazon, Yahoo

Cluster 2: Comcast, Cablevision, Time Warner

Cluster 3: ConocoPhillips, Chevron, Total, Valero Energy, Exxon

Cluster 4: Cisco, Dell, HP, IBM, Microsoft, SAP, Texas Instruments

Cluster 5: Boeing, General Dynamics, Northrop Grumman, Raytheon

Cluster 6: AIG, American express, Bank of America, Caterpillar, CVS, DuPont de Nemours, Ford, General Electrics, Goldman Sachs, Home Depot, JPMorgan Chase, Marriott, McDonald's, 3M, Ryder, Wells Fargo, Wal-Mart

Cluster 7: GlaxoSmithKline, Novartis, Pfizer, Sanofi-Aventis, Unilever

Cluster 8: Kellogg, Coca Cola, Pepsi

Cluster 9: Colgate-Palmolive, Kimberly-Clark, Procter Gamble

Cluster 10: Canon, Honda, Navistar, Sony, Toyota, Xerox

Embedding in 2D space#

For visualization purposes, we need to lay out the different symbols on a 2D canvas. For this we use Manifold learning techniques to retrieve 2D embedding. We use a dense eigen_solver to achieve reproducibility (arpack is initiated with the random vectors that we don’t control). In addition, we use a large number of neighbors to capture the large-scale structure.

# Finding a low-dimension embedding for visualization: find the best position of

# the nodes (the stocks) on a 2D plane

from sklearn import manifold

node_position_model = manifold.LocallyLinearEmbedding(

n_components=2, eigen_solver="dense", n_neighbors=6

)

embedding = node_position_model.fit_transform(X.T).T

Visualization#

The output of the 3 models are combined in a 2D graph where nodes represents the stocks and edges the:

cluster labels are used to define the color of the nodes

the sparse covariance model is used to display the strength of the edges

the 2D embedding is used to position the nodes in the plan

This example has a fair amount of visualization-related code, as visualization is crucial here to display the graph. One of the challenge is to position the labels minimizing overlap. For this we use an heuristic based on the direction of the nearest neighbor along each axis.

import matplotlib.pyplot as plt

from matplotlib.collections import LineCollection

plt.figure(1, facecolor="w", figsize=(10, 8))

plt.clf()

ax = plt.axes([0.0, 0.0, 1.0, 1.0])

plt.axis("off")

# Plot the graph of partial correlations

partial_correlations = edge_model.precision_.copy()

d = 1 / np.sqrt(np.diag(partial_correlations))

partial_correlations *= d

partial_correlations *= d[:, np.newaxis]

non_zero = np.abs(np.triu(partial_correlations, k=1)) > 0.02

# Plot the nodes using the coordinates of our embedding

plt.scatter(

embedding[0], embedding[1], s=100 * d**2, c=labels, cmap=plt.cm.nipy_spectral

)

# Plot the edges

start_idx, end_idx = np.where(non_zero)

# a sequence of (*line0*, *line1*, *line2*), where::

# linen = (x0, y0), (x1, y1), ... (xm, ym)

segments = [

[embedding[:, start], embedding[:, stop]] for start, stop in zip(start_idx, end_idx)

]

values = np.abs(partial_correlations[non_zero])

lc = LineCollection(

segments, zorder=0, cmap=plt.cm.hot_r, norm=plt.Normalize(0, 0.7 * values.max())

)

lc.set_array(values)

lc.set_linewidths(15 * values)

ax.add_collection(lc)

# Add a label to each node. The challenge here is that we want to

# position the labels to avoid overlap with other labels

for index, (name, label, (x, y)) in enumerate(zip(names, labels, embedding.T)):

dx = x - embedding[0]

dx[index] = 1

dy = y - embedding[1]

dy[index] = 1

this_dx = dx[np.argmin(np.abs(dy))]

this_dy = dy[np.argmin(np.abs(dx))]

if this_dx > 0:

horizontalalignment = "left"

x = x + 0.002

else:

horizontalalignment = "right"

x = x - 0.002

if this_dy > 0:

verticalalignment = "bottom"

y = y + 0.002

else:

verticalalignment = "top"

y = y - 0.002

plt.text(

x,

y,

name,

size=10,

horizontalalignment=horizontalalignment,

verticalalignment=verticalalignment,

bbox=dict(

facecolor="w",

edgecolor=plt.cm.nipy_spectral(label / float(n_labels)),

alpha=0.6,

),

)

plt.xlim(

embedding[0].min() - 0.15 * np.ptp(embedding[0]),

embedding[0].max() + 0.10 * np.ptp(embedding[0]),

)

plt.ylim(

embedding[1].min() - 0.03 * np.ptp(embedding[1]),

embedding[1].max() + 0.03 * np.ptp(embedding[1]),

)

plt.show()

Total running time of the script: (0 minutes 6.677 seconds)

Related examples

Manifold learning on handwritten digits: Locally Linear Embedding, Isomap…

Various Agglomerative Clustering on a 2D embedding of digits