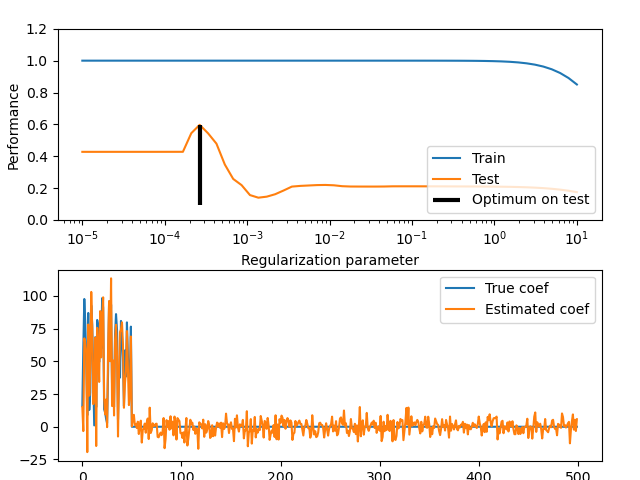

Train error vs Test error#

Illustration of how the performance of an estimator on unseen data (test data) is not the same as the performance on training data. As the regularization increases the performance on train decreases while the performance on test is optimal within a range of values of the regularization parameter. The example with an Elastic-Net regression model and the performance is measured using the explained variance a.k.a. R^2.

# Author: Alexandre Gramfort <alexandre.gramfort@inria.fr>

# License: BSD 3 clause

Generate sample data#

import numpy as np

from sklearn import linear_model

from sklearn.datasets import make_regression

from sklearn.model_selection import train_test_split

n_samples_train, n_samples_test, n_features = 75, 150, 500

X, y, coef = make_regression(

n_samples=n_samples_train + n_samples_test,

n_features=n_features,

n_informative=50,

shuffle=False,

noise=1.0,

coef=True,

)

X_train, X_test, y_train, y_test = train_test_split(

X, y, train_size=n_samples_train, test_size=n_samples_test, shuffle=False

)

Compute train and test errors#

alphas = np.logspace(-5, 1, 60)

enet = linear_model.ElasticNet(l1_ratio=0.7, max_iter=10000)

train_errors = list()

test_errors = list()

for alpha in alphas:

enet.set_params(alpha=alpha)

enet.fit(X_train, y_train)

train_errors.append(enet.score(X_train, y_train))

test_errors.append(enet.score(X_test, y_test))

i_alpha_optim = np.argmax(test_errors)

alpha_optim = alphas[i_alpha_optim]

print("Optimal regularization parameter : %s" % alpha_optim)

# Estimate the coef_ on full data with optimal regularization parameter

enet.set_params(alpha=alpha_optim)

coef_ = enet.fit(X, y).coef_

Optimal regularization parameter : 0.0002652948464431897

Plot results functions#

import matplotlib.pyplot as plt

plt.subplot(2, 1, 1)

plt.semilogx(alphas, train_errors, label="Train")

plt.semilogx(alphas, test_errors, label="Test")

plt.vlines(

alpha_optim,

plt.ylim()[0],

np.max(test_errors),

color="k",

linewidth=3,

label="Optimum on test",

)

plt.legend(loc="lower right")

plt.ylim([0, 1.2])

plt.xlabel("Regularization parameter")

plt.ylabel("Performance")

# Show estimated coef_ vs true coef

plt.subplot(2, 1, 2)

plt.plot(coef, label="True coef")

plt.plot(coef_, label="Estimated coef")

plt.legend()

plt.subplots_adjust(0.09, 0.04, 0.94, 0.94, 0.26, 0.26)

plt.show()

Total running time of the script: (0 minutes 6.953 seconds)

Related examples

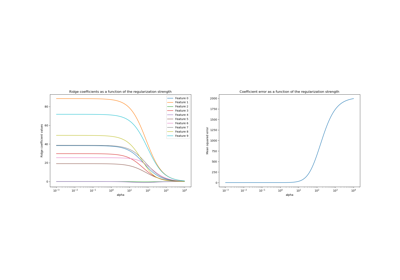

Ridge coefficients as a function of the L2 Regularization

Ridge coefficients as a function of the L2 Regularization